Taxpayers planning for the 2025 filing season face an evolving landscape. Deloitte’s 2025 tax guide warns that policy shifts—especially the potential expiration of many Tax Cuts and Jobs Act provisions—require keeping an eye on the horizon. At the same time, the IRS has received billions of dollars to step up enforcement, making proactive planning more important than ever.

Standard deduction and tax brackets

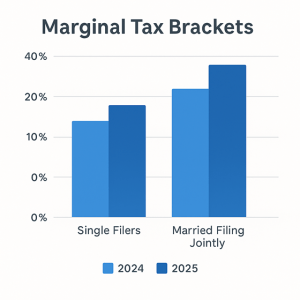

One of the biggest changes in 2025 is the increase in the standard deduction. KPMG’s planning guide notes that for the 2024 tax year the standard deduction was $14,600 for single filers, $21,900 for heads of household, and $29,200 for married couples filing jointly. Fidelity reports that in 2025 these amounts rise to $15,000 for single filers and $30,000 for married couples filing jointly. Because the standard deduction eliminates tax on the first slice of income, many taxpayers will find that itemizing deductions is no longer worthwhile.

Inflation adjustments also widen tax brackets, meaning more income can be taxed at lower rates. The marriage penalty—where joint filers pay more tax than two singles—now only affects couples whose combined taxable income exceeds $731,200. Head‑of‑household filers, who must be unmarried and provide a home for a qualifying dependent, enjoy a higher standard deduction and lower rates. Understanding whether you qualify can save you hundreds or even thousands of dollars.

Why planning matters

Although the 2025 standard deduction has increased, the cap on state and local tax (SALT) deductions remains $10,000. Taxpayers in high‑tax states who own homes may still benefit from itemizing deductions and bundling charitable donations. Moreover, personal exemptions remain suspended through 2025, so families should ensure they claim all available credits, such as the child tax credit.

Another important factor is your filing status. Head‑of‑household status is reserved for unmarried taxpayers who support a dependent child or relative and pay more than half the cost of maintaining the household. This status offers a higher standard deduction and lower tax brackets than single status. Understanding whether you qualify can make a significant difference in your tax bill.

The marriage penalty has been alleviated for most taxpayers. KPMG observes that the joint tax brackets for married filers are double those for single filers, so the penalty only applies when combined taxable income exceeds $731,200. Even so, couples should run the numbers both ways (jointly and separately) to determine the most tax‑efficient filing method.

Federal tax law is scheduled for major changes after 2025, as many TCJA provisions expire. Without legislative action, marginal tax rates will rise and estate‑tax exemptions will shrink. By planning now—reviewing your income, credits, deductions and potential exposure to the SALT cap—you can make informed choices about withholding and estimated tax payments. Proactive planning also positions you to react quickly to any changes enacted by Congress.